October 20, 2016Taxes5 min read

I live in Kansas but work in Missouri

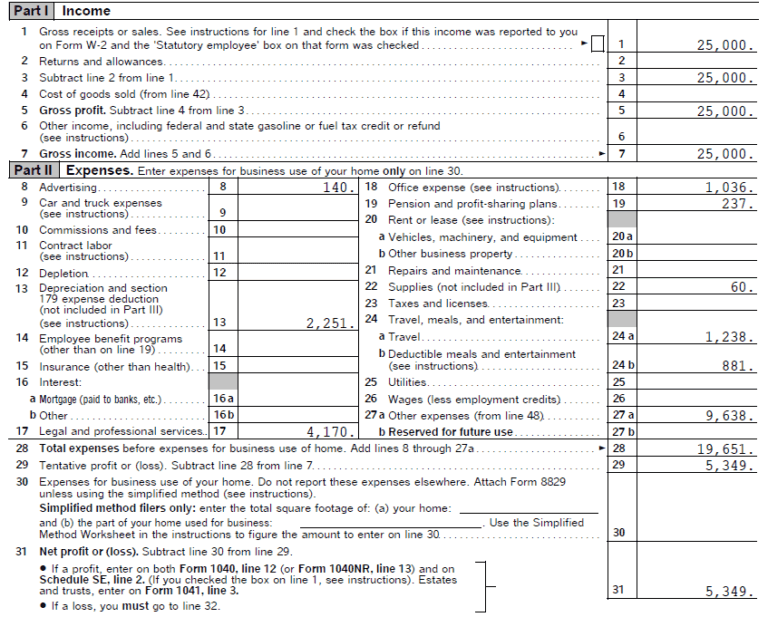

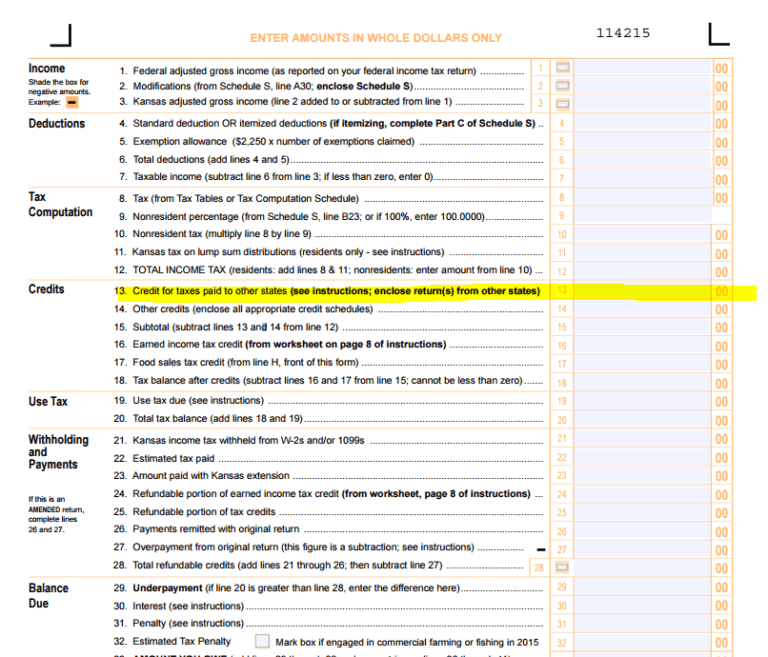

Filing in multiple states is common and doesn't necessarily mean double taxation. If you live in one state (like Kansas) but work in another (like Missouri), you generally receive a **credit for taxes paid to other states**. To avoid double taxation, first complete your federal and nonresident state returns. Then, take the tax liability from the nonresident return and apply it as a credit on your home state return. This mechanism ensures you only pay the higher of the two rates.